Are you or someone you know in debt? It’s 2020. Of course you or someone you know id in debt. What if I told you that if you have more than 1 debt, there is an optimal way to pay off your debts that will help you pay the debt off as quickly as inexpensively as possible? Have you heard of the Snowball Method or the Avalanche Method of paying off debt? The Snowball Method and the Avalanche Method are simple to calculate and follow, and will help you get out of debt quicker than any other way.

Some financial experts will usually recommend only one of these two methods, especially the Snowball Method, but it isn’t always one size fits all. With a little bit of math, you can figure out which method is best for you.

Using math to get out of debt

MATH??!?!? DID YOU SAY MATH?!?!?!?

Don’t worry. I am your FinancuallySavvyParent. I love you, and I am not going to let anything, especially math, come between you, and your financial freedom.

There are online calculators, so you don’t even have to do that math. I am going to share a link to a website that will allow you to run both the snowball and avalanche method, so you can figure out the best way to pay off your debt.

Gathering info about our debts

For either of the methods, you are going to need to know a few pieces of info, all of which you can find on your credit card or loan statement:

- What the minimum payments on each of your cards/loans is.

- What the total amount owed on each of those debts

- The interest rate of each of those debts

One more thing you need to know is how much EXTRA you are willing to put toward your debt. For example, in addition to all of the minimum payments, you are planning to put an additional $100 or $200 towards your debts monthly. This extra amount is SUPER important. You can’t just pay the minimum, or it will waaaaay too long to pay these debts off. Figure out some amount or additional money you are putting towards your debts. Literally any amount helps, and the more the merrier.

Once you have that, let’s double down and learn about the methods.

Snowball Method

First up is the Snowball method. With the snowball method you start by arranging all of your debts from the smallest amount owed to the largest amount owed. You are going to pay the minimum + the extra towards the smallest debt. For all the others you are going to pay the minimum. As you pay down the first debt, the minimum payment will lessen. Resist the temptation to pay less per month. We are on the road to recovery!

You will pay the same amount each month towards the first debt, and same goes for the other minimums. From today forward, these minimums are the least we are going to pay on these debts. If we go lower, things will take longer and cost more. Lock all these minimum payments in today.

So when you pay off the first debt, you no longer have that 1st minimum payment. Do we pay less now per month? NO! Of course not! We roll that over to the second debt. That means for the second debt we are now paying the minimum of your 1st debt + the minimum of your 2nd debt + your extra amount. You are making a bigger snowball to pay towards you debt.

Pay off that 2nd debt and you will have an even larger amount to throw at that smaller debt. Keep going until you are out of debt. This could take years, but if we don’t follow a plan, it will take years and then some, and would cost you even more.

Avalanche Method

The second method is the Avalanche Method, and we are going to sort the debts by the highest interest rate. The Snowball Method was sorted by debt balances, from highest to lowest. For the avalanche method, we are sorting by interest rates, from highest to lowest.

The same applies here. Pay the minimum plus the extra payment towards the debt with the highest interest rate. You pay minimums on the others. Then, when the first debt is done you pay 1st minimum + 2nd minimum + the extra towards the next debt, and so on and so forth.

With the Avalanche Method you are slowing down the effects of compound interest, which is one of the most powerful forces in the universe.

For the sake of understanding, we are going to use some sample numbers. I am going to make the explanation very light on the numbers, so we don’t get bogged down. We are going to let the website do the math, so fear not. Remember, I am your FinanciallySavvyParent. I am here for you!

Paying off debts – An example

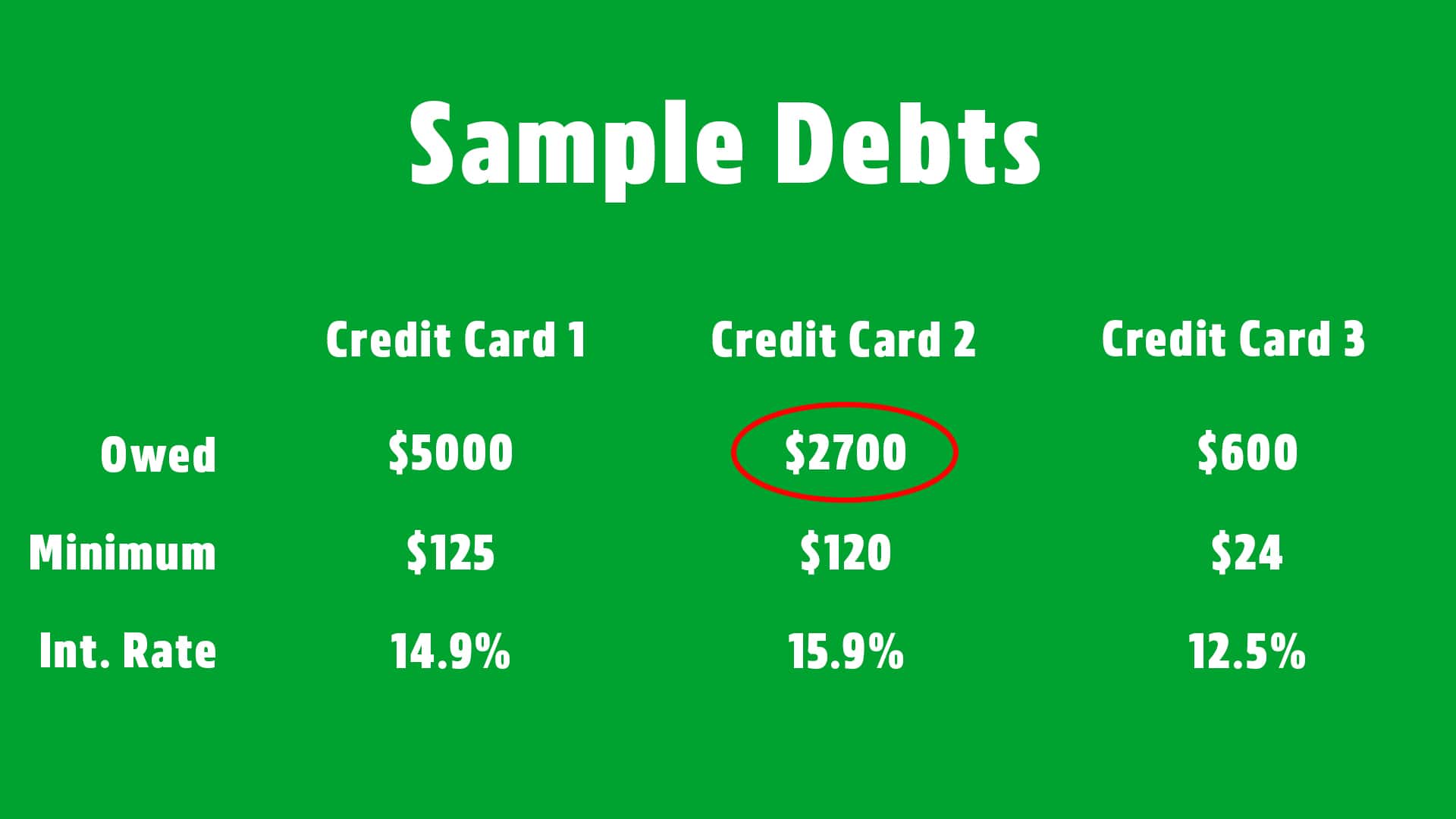

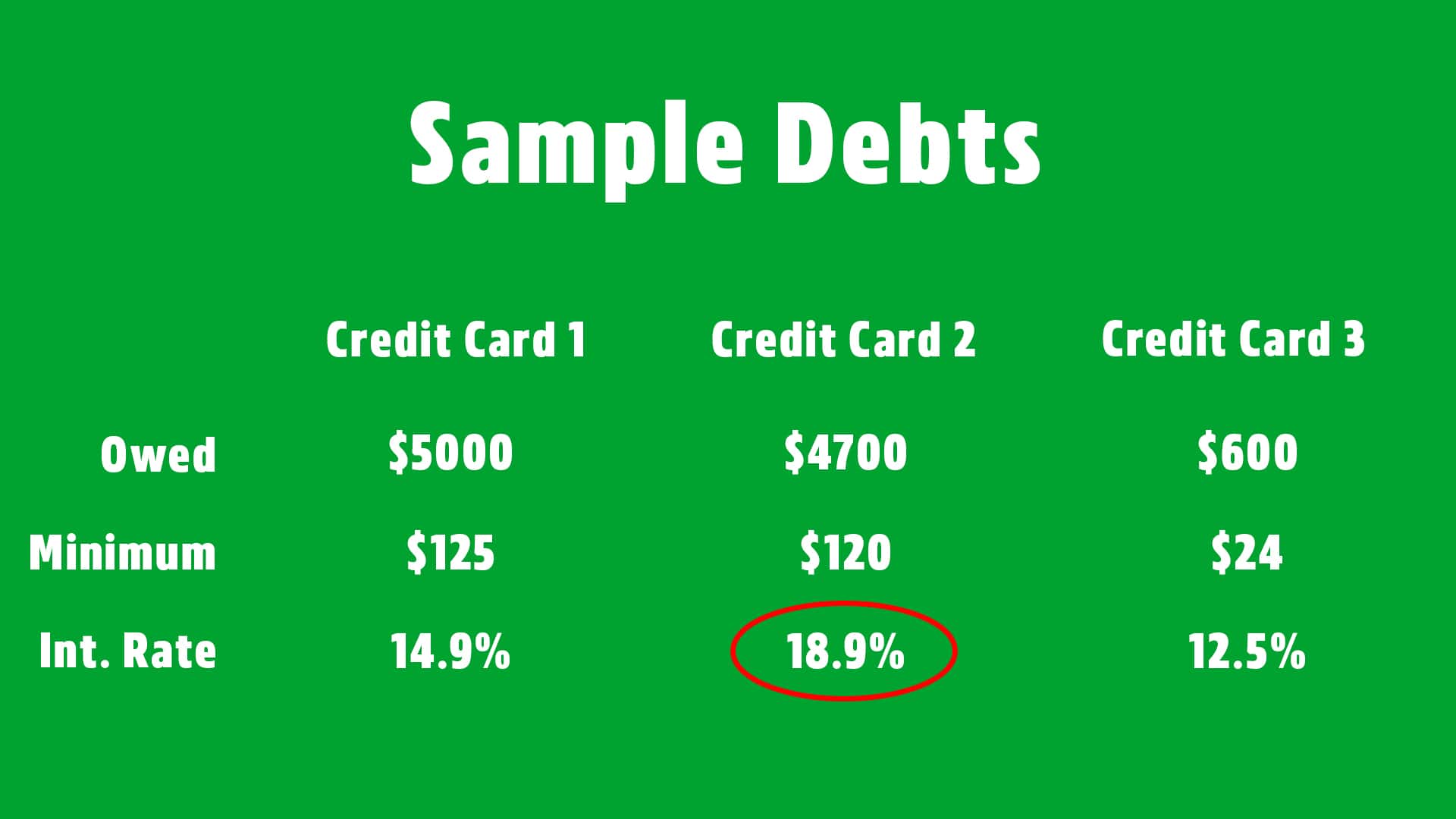

Here are our sample debts:

Some time not too long ago, the credit card companies let us have more credit than we knew how to be responsible for, so now we have some debts:

First is a credit card with a balance of $5000. We maxed it out. The minimum monthly payment is $125/month. The annual interest rate is 14.9%.

Up next is the second card we maxed out, at $4700. The minimum monthly payment is $120, and the annual interest rate is 15.9%.

Our final one is the only one we didn’t max out (yet) with a balance of $600. The minimum monthly payment is $24, and the annual interest rate is 12.5%.

OK. Time out! So, we are in debt. That is the past! Now we are listening and learning from out Financially Savvy Parent, and we are working to get out of debt. So how do we do it as fast and as painlessly as possible?

Let’s head over to undebt.it and go to their calendar. (https://undebt.it/debt-snowball-calculator.php).

Running our test numbers

So, fill in each of the three debts, one per row. You can make the account name anything you want. I used CC 1, 2, and 3. One thing I like about this calculator is that it allows you to fill in the total amount you want to use to pay towards debt. It keeps that amount constant. If it did not remain constant, the total amount you spent each month would go down as you pay down your debts. You’d still be paying your debts, but just not as fast. With the constant debt payments, you actually start hitting the balances harder each month relative to the amount owed.

With these sample numbers, I ran the Snowball Method and the Avalanche Method to see who would win. There are some other methods you can try. Maybe one will be better for you.

Running Snowball vs. Avalanche, we can see that Avalanche won by $27.62. That means if you paid off your highest rates first, rather than your smallest debts first, with these sample numbers, you would save $27.62. Remember, your numbers will be different. These are just some samples. Run your numbers and see which works best for you.

Snowball vs. Avalanche – Round 2

Now I wanted to make some changes and see how the tests play out. In the 2nd test, I dropped CC2 down to just $2700. Will the Avalanche Method still win? If so, by how much?

Turns out, when we use out handy dandy calculator, in this round, the Avalanche Method wins yet again! This time by $25.57. Avalanche is 2 for 2!

Snowball vs. Avalanche – Round 3 – Final Round

For the 3rd and final test, we are doing to rest set out numbers, and this time increase the interest rate of CC 2 all the way up to 18.9%. If you have had some trouble, your interest rates could be this or higher, so let’s see how this works out.

With a little quick handy dandy math done by the website, turns out, drum roll please. (Drum roll sound effect)

The winner is the Avalanche method! How did the Avalanche Method win 3 for 3? The answer is simple. It’s just math. The Avalanche Method focuses on wiping out the debt with the highest interest rates first. Interest rates, and the compound interest they produce, is the source of growth. The Avalanche Method’s purpose is to slow down and then kill the growth of the debt as much as possible. If you kill the source of growth, your payments can make a greater impact each month than if the compound interest were growing faster.

So if the Avalanche Method works so well, why do other experts recommend the Snowball Method? I believe the answer is also simple. When we work with the Avalanche Method, we are focusing solely on the numbers, and paying of debt as fast as possible, paying the least we can. With our sample numbers, how long did it take to pay off each the first credit card each time? It took 25 months in the first example. 14 months int he second example. 27 months in the third example.

With the Snowball Method, it took 5 months, 4 months, and 5 months, respectively, to pay off the first card in each example. That means about 4 to 5 months in you have a small win under your belt, and you are feeling great. Early on, you have some positive reinforcement that your cost cutting and budgeting can really make a difference. With the Avalanche Method, you don’t get that positive reinforcement for a year or two.

Then, when all is said and done how much do you save by going with the Avalanche Method? Somewhere between $25 and $200. If you look solely at the numbers, Avalanche wins, but with Snowball, you get that emotional encouragement, which can make a big difference for us when we are going through such big changes in our lives.

Final Thoughts

It is up to you to run the math and see which method fits your financial situation best. Even when doing the math, remember to consider which method would work best for you, knowing how you handle situations emotionally. Whichever you pick, stick to the plan. Just as you got yourself into trouble, you can get yourself out, and these two methods can help you get on track to be out of debt, and then onto much more exciting financial ventures.

Nadav

Related lessons

The Big Idea Most people spend first and save whatever is left over. Successful savers do the opposite.…

Who the heck wants to save money? Spending vs Saving is a real struggle. Few normal people wake…

If you are thinking about giving your child an allowance, but aren’t sure the best way to do…